How To Get The Most Out Of Your Health Insurance Coverage — Strategies You Can Use Right Now, And At Your Next Enrollment

Using your insurance is a great way to get the help you need without breaking the bank. Unfortunately, insurance companies like to be difficult, and they are constantly coming up with new ways to be complicated.

Disclaimer: I am writing this from the perspective of a healthcare consumer and a healthcare provider. I am not an insurance professional and am not offering professional advice. If you need professional insurance advice, please consult with a licensed broker.

First, Some Insurance Vocabulary

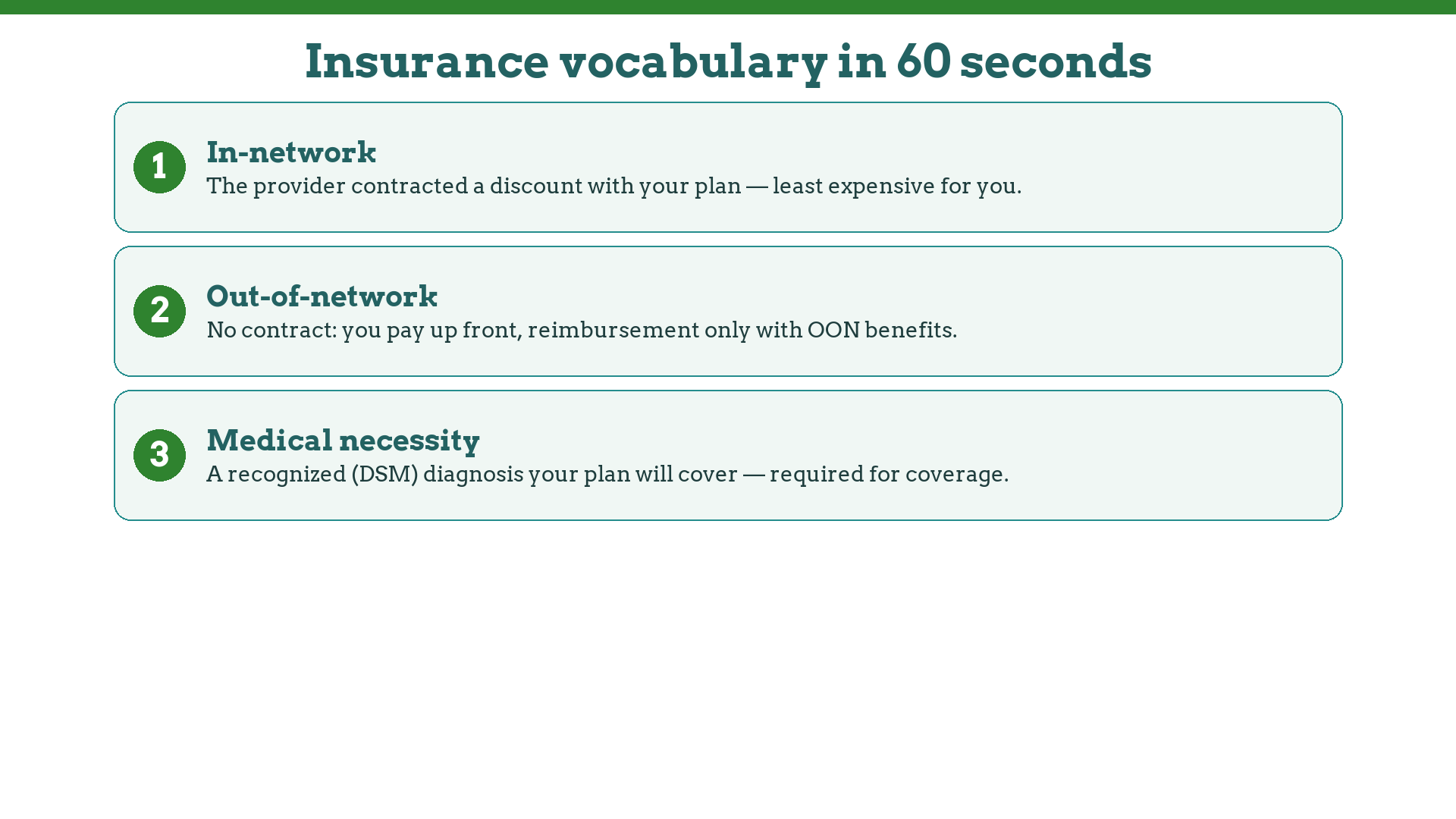

What does In-Network mean?

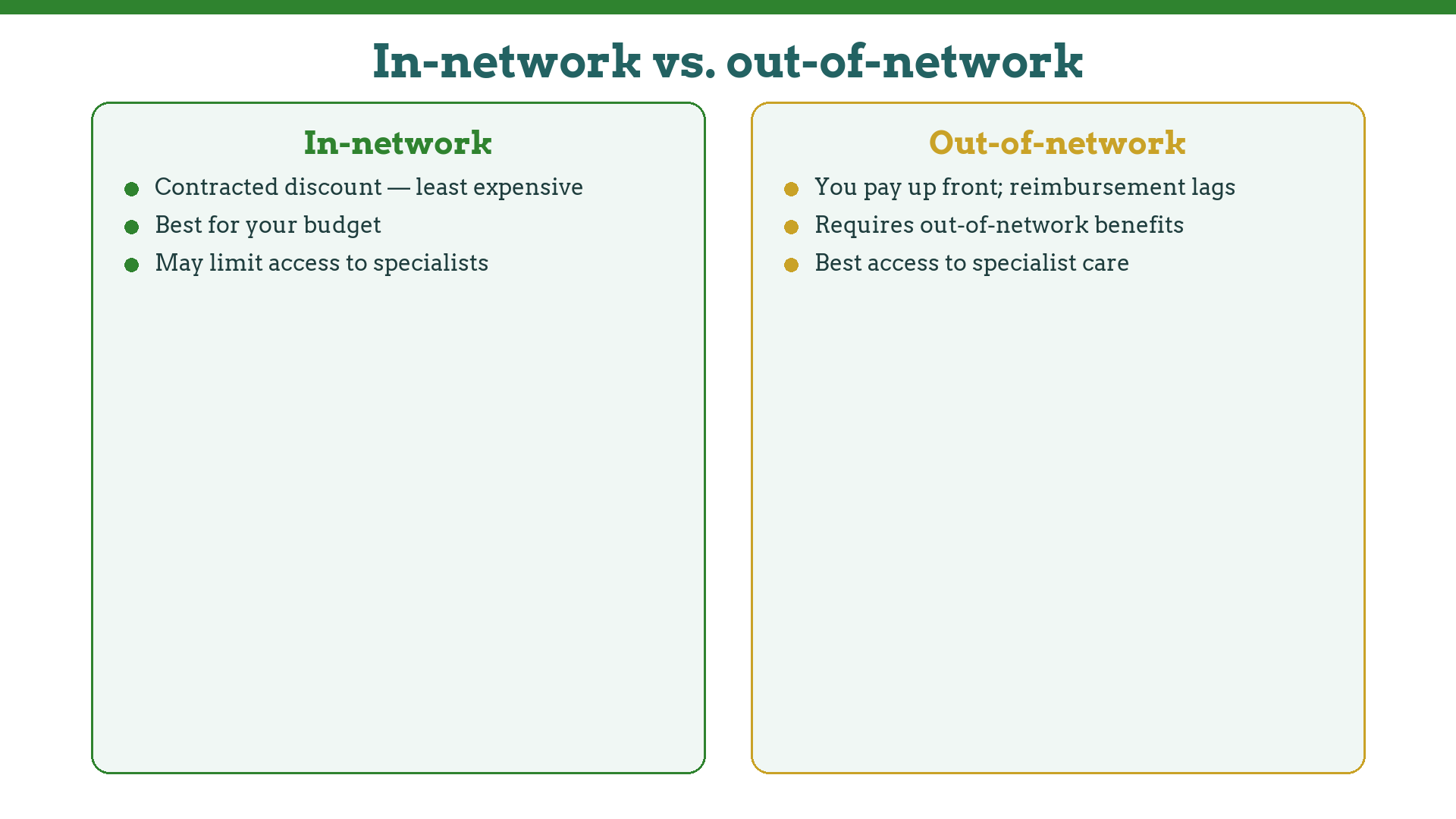

A healthcare provider is “in-network” when they have signed an agreement with your health plan to offer their services to members of that carrier’s network for a discount. This discount may be as high as 50% off of otherwise fair market pricing. The discount can make it hard for specialist providers to offer their services in-network because of the higher costs they pay for continuing education and certifications in their specialties.

In-network coverage for medical care is best for your budget because it’s the least expensive. However, it may not be the best for your quality of care if you need to see a specialist instead of a general provider.

What does Out-of-Network mean?

A healthcare provider is “out-of-network” when they have not signed an agreement with your insurance carrier. This means that you will be responsible for paying for services, and the provider may or may not help you pursue reimbursement from your insurance for part or all of the cost. You must have out-of-network coverage on your plan to get reimbursed for any expenses.

Out-of-network coverage may be unaffordable because you will pay more for your care, and even if you have out-of-network benefits, there will be a lag between when you pay for services and when you get reimbursed. However, it may improve your quality of care by allowing you to work with a specialist.

What does Medical Necessity mean?

The services must be medically necessary to have your insurance pay for your healthcare services. Your healthcare provider must diagnose you with a recognized health condition. For mental health services, a provider must diagnose you with a disorder listed in the DSM-V-TR. Your healthcare provider must also provide your insurance carrier with enough information to support the diagnosis.

Medical Necessity may create problems when:

- You are seeking couple or family therapy because the DSM-V-TR does not list couples or family issues as primary mental health issues but rather as “Z-Codes,” which indicate the context(s) in which other challenges are occurring. There is currently no recognition in the DSM or by insurance companies that contexts interact with otherwise covered disorders.

- You are seeking help with challenges that the DSM does not recognize. Porn addiction, sex addiction, or betrayal trauma, for example.

- You are seeking services that your insurance carrier does not believe are “indicated” for the diagnoses in your medical record.

What is a Single Patient Authorization?

If you cannot find an in-network provider who can help you with your challenges, you may be able to get a Single Patient Authorization. These are very hard to get. You will need to call the member services department of your insurance carrier and ask them how the process works for your specific plan and carrier. No two plans or carriers are the same. Most often, if this is an option, your primary care doctor and your mental health provider will need to collaborate to pull this off. Any costs of services that you received before the authorization were in place will not be reimbursed.

What is a Copay?

Copays are your part of the fee for healthcare services for in-network providers. Your insurance carrier pays the rest. Copays may be reduced or eliminated after your deductible is met, depending on the specifics of your plan and carrier. Copays can be a challenge for some people who are on high deductible plans where insurance only pays for services after the deductible has been met.

What is a Coinsurance Fee?

Coinsurance fees are your part of the fee for healthcare services for out-of-network providers. Your insurance carrier pays the rest. These fees may be reduced or eliminated after your deductible has been met. Some plans and carriers also use this term for the reduced fees that you pay after your deductible has been met.

What is a Deductible?

A deductible is a specified dollar amount when your costs for healthcare services will change. Most plans will cover a more significant portion of healthcare costs after the deductible has been met. Meeting your deductible will not necessarily eliminate all copays or coinsurance fees, but it will usually reduce them. You pay your copays, coinsurance fees, or other plan-approved expenses to meet your deductible. The insurance carrier will use claims to keep a running total of what you have spent toward your deductible.

What is an Out-of-pocket-max?

An out-of-pocket-max is a specified dollar amount when your costs for healthcare services will change again. Most plans will cover all your plan-approved healthcare costs after the out-of-pocket max has been reached.

What is a Health Savings Account (HSA)?

A Health Savings Account, or HSA, is a feature offered with some health insurance plans which provides you with a debit or credit card to use for plan-approved expenses. Some plans will use your HSA spending instead of the claims they receive to track when you meet your deductible and out-of-pocket-max. HSA’s may also have tax benefits, and you can keep what you don’t spend for future health spending. Consult with a tax advisor or insurance advisor to see whether this sort of plan is best for you.

What is an Explanation of Benefits (EOB)?

An Explanation of Benefits, or EOB, is a statement addressing one or more dates of service, and one or more types of health care costs (services, medications, devices, etc). It will explain:

- Which healthcare providers rendered the services.

- Whether they are in-network or out-of-network.

- What copays or coinsurance fees were paid (or are owed).

- What the health insurance provider has paid.

- What the health care providers charged for the services.

- What adjustments (discounts) were made by the insurance company.

Strategies to Get The Most Out Of Your Insurance

There are many strategies to help you get the most out of health insurance. You should always check with your doctor before making any changes to your medical care. If you need to change doctors, ask about switching plans. Your plan may offer discounts if you switch providers. Not all of these strategies apply to everyone. But most people will be able to use at least one or two.

Shop Wisely, and Get Help Shopping

Work with a licensed broker to select your insurance plan.

When you enroll in your health insurance every year, ensure you understand your copays, deductible, and out-of-pocket-max.

Get a health insurance plan with an HSA feature if your employer offers one.

If you cannot choose health coverage with an HSA feature, ensure an emergency fund to cover unplanned health expenses.

Know the Details of Your Plan

Read your plan’s coverage documents every year – even if you think you know what they say. Health insurance is complex. You need to know what’s in your plan before you can use it. At the beginning of every year, take a few moments to review your health insurance plan. Make sure you understand any changes that will affect you and your family. If there are any changes, ask questions about them.

Get a list of all of your plan-approved expenses. When you buy a plan-approved item or pay for a plan-approved service, ensure that only plan-approved expenses are on that purchase, and keep your receipt. Contact your plan’s member services department to determine how to submit those receipts to count toward your deductible.

You should check your benefits if your health changes. Things that weren’t important to you before might become important, like coverage for doctors or prenatal benefits. If you’re not sure whether you need to change your plan, ask your doctor or call the company directly. You can also get free help at healthcare.gov.

Find a Good Primary Care Provider (PCP)

Your PCP is often the gatekeeper to screenings, preventative care options, and specialist referrals.

A good PCP will know your family history, your lifestyle habits, and your baseline vital signs. They will also help you stay healthy by flagging screenings you might be eligible for, spotting issues early, and directing you to a specialist if you need one.

Take advantage of preventive care

Some plans make preventative care available for free or very low cost, and then make access to specialists easier if you have already taken advantage of the preventative options they offer.

Plan the Timing of Procedures Strategically

You can’t plan for emergencies like appendicitis, but you can be smart about scheduling surgeries and other health care needs. If possible, plan expensive procedures after your deductible or out-of-pocket-max have already been met.

Learn How to File a Claim

If you are going out-of-network for higher quality care, you will need to ask the provider for a superbill. You will then need to contact member services at your medical insurance to learn how to submit the superbill so that you can get reimbursed.

Don’t miss out on perks

In the United States, we have to juggle so many things just to get — and understand — basic health coverage. We have to pay out of pocket for everything from doctor visits to prescriptions to hospital bills. And even when we have insurance, there are still so many hoops to jump through before we can actually access our benefits. But despite all of those financial and logistical headaches, your insurance plan might come with some nice perks too. Want to take Zumba classes? Your insurance provider might offer discounts if you join a local gym membership. Or it could offer discounts on services that help you stay healthy, like laser eye surgery or massages. If you’re taking medications, your insurer might give you a discount at its preferred pharmacy, or let you shop around online for other providers or facilities for the medical care that you need.

Save and share

Pin or share these — someone you love may need them today.

Next Steps

If you’re ready, you can get started with counseling at Restored Life. Or, if you’re not sure whether you need counseling, take the free survey to screen for the most common mental health challenges that people face.